if(par3!='NA') par3 <- as.numeric(par3) else par3 <- NA

if(par4!='NA') par4 <- as.numeric(par4) else par4 <- NA

par6 <- as.numeric(par6) #Seasonal Period

par9 <- as.numeric(par9) #Forecast Horizon

par10 <- as.numeric(par10) #Alpha

library(forecast)

if (par1 == 'CSV') {

xarr <- read.csv(file=paste('tmp/',par7,'.csv',sep=''),header=T)

numseries <- length(xarr[1,])-1

n <- length(xarr[,1])

nmh <- n - par9

nmhp1 <- nmh + 1

rarr <- array(NA,dim=c(n,numseries))

farr <- array(NA,dim=c(n,numseries))

parr <- array(NA,dim=c(numseries,8))

colnames(parr) = list('ME','RMSE','MAE','MPE','MAPE','MASE','ACF1','TheilU')

for(i in 1:numseries) {

sindex <- i+1

x <- xarr[,sindex]

if(par2=='Croston') {

if (i==1) m <- croston(x,alpha=par10)

if (i==1) mydemand <- m$model$demand[]

fit <- croston(x[1:nmh],h=par9,alpha=par10)

}

if(par2=='ARIMA') {

m <- auto.arima(ts(x,freq=par6),d=par3,D=par4)

mydemand <- forecast(m)

fit <- auto.arima(ts(x[1:nmh],freq=par6),d=par3,D=par4)

}

if(par2=='ETS') {

m <- ets(ts(x,freq=par6),model=par5)

mydemand <- forecast(m)

fit <- ets(ts(x[1:nmh],freq=par6),model=par5)

}

try(rarr[,i] <- mydemand$resid,silent=T)

try(farr[,i] <- mydemand$mean,silent=T)

if (par2!='Croston') parr[i,] <- accuracy(forecast(fit,par9),x[nmhp1:n])

if (par2=='Croston') parr[i,] <- accuracy(fit,x[nmhp1:n])

}

write.csv(farr,file=paste('tmp/',par8,'_f.csv',sep=''))

write.csv(rarr,file=paste('tmp/',par8,'_r.csv',sep=''))

write.csv(parr,file=paste('tmp/',par8,'_p.csv',sep=''))

}

if (par1 == 'Input box') {

numseries <- 1

n <- length(x)

if(par2=='Croston') {

m <- croston(x)

mydemand <- m$model$demand[]

}

if(par2=='ARIMA') {

m <- auto.arima(ts(x,freq=par6),d=par3,D=par4)

mydemand <- forecast(m)

}

if(par2=='ETS') {

m <- ets(ts(x,freq=par6),model=par5)

mydemand <- forecast(m)

}

summary(m)

}

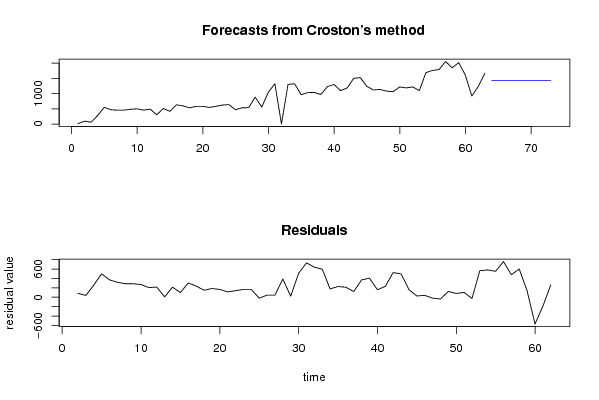

bitmap(file='test1.png')

op <- par(mfrow=c(2,1))

if (par2=='Croston') plot(m)

if ((par2=='ARIMA') | par2=='ETS') plot(forecast(m))

plot(mydemand$resid,type='l',main='Residuals', ylab='residual value', xlab='time')

par(op)

dev.off()

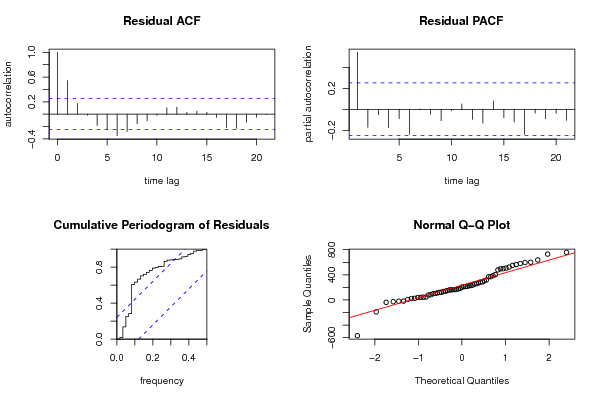

bitmap(file='pic2.png')

op <- par(mfrow=c(2,2))

acf(mydemand$resid, lag.max=n/3, main='Residual ACF', ylab='autocorrelation', xlab='time lag')

pacf(mydemand$resid,lag.max=n/3, main='Residual PACF', ylab='partial autocorrelation', xlab='time lag')

cpgram(mydemand$resid, main='Cumulative Periodogram of Residuals')

qqnorm(mydemand$resid); qqline(mydemand$resid, col=2)

par(op)

dev.off()

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Demand Forecast',6,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Point',header=TRUE)

a<-table.element(a,'Forecast',header=TRUE)

a<-table.element(a,'95% LB',header=TRUE)

a<-table.element(a,'80% LB',header=TRUE)

a<-table.element(a,'80% UB',header=TRUE)

a<-table.element(a,'95% UB',header=TRUE)

a<-table.row.end(a)

for (i in 1:length(mydemand$mean)) {

a<-table.row.start(a)

a<-table.element(a,i+n,header=TRUE)

a<-table.element(a,as.numeric(mydemand$mean[i]))

a<-table.element(a,as.numeric(mydemand$lower[i,2]))

a<-table.element(a,as.numeric(mydemand$lower[i,1]))

a<-table.element(a,as.numeric(mydemand$upper[i,1]))

a<-table.element(a,as.numeric(mydemand$upper[i,2]))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'What is next?',1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,hyperlink(paste('https://automated.biganalytics.eu/Patrick.Wessa/rwasp_demand_forecasting_simulate.wasp',sep=''),'Simulate Time Series','',target=''))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,hyperlink(paste('https://automated.biganalytics.eu/Patrick.Wessa/rwasp_demand_forecasting_croston.wasp#output',sep=''),'Generate Forecasts','',target=''))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,hyperlink(paste('https://automated.biganalytics.eu/Patrick.Wessa/rwasp_demand_forecasting_analysis.wasp',sep=''),'Forecast Analysis','',target=''))

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable0.tab')

-SERVER-wessa.org

|