par1 <- as.numeric(par1) #cut off periods

par2 <- as.numeric(par2) #lambda

par3 <- as.numeric(par3) #degree of non-seasonal differencing

par4 <- as.numeric(par4) #degree of seasonal differencing

par5 <- as.numeric(par5) #seasonal period

par6 <- as.numeric(par6) #p

par7 <- as.numeric(par7) #q

par8 <- as.numeric(par8) #P

par9 <- as.numeric(par9) #Q

if (par10 == 'TRUE') par10 <- TRUE

if (par10 == 'FALSE') par10 <- FALSE

if (par2 == 0) x <- log(x)

if (par2 != 0) x <- x^par2

lx <- length(x)

first <- lx - 2*par1

nx <- lx - par1

nx1 <- nx + 1

fx <- lx - nx

if (fx < 1) {

fx <- par5

nx1 <- lx + fx - 1

first <- lx - 2*fx

}

first <- 1

if (fx < 3) fx <- round(lx/10,0)

(arima.out <- arima(x[1:nx], order=c(par6,par3,par7), seasonal=list(order=c(par8,par4,par9), period=par5), include.mean=par10, method='ML'))

(forecast <- predict(arima.out,par1))

(lb <- forecast$pred - 1.96 * forecast$se)

(ub <- forecast$pred + 1.96 * forecast$se)

if (par2 == 0) {

x <- exp(x)

forecast$pred <- exp(forecast$pred)

lb <- exp(lb)

ub <- exp(ub)

}

if (par2 != 0) {

x <- x^(1/par2)

forecast$pred <- forecast$pred^(1/par2)

lb <- lb^(1/par2)

ub <- ub^(1/par2)

}

if (par2 < 0) {

olb <- lb

lb <- ub

ub <- olb

}

(actandfor <- c(x[1:nx], forecast$pred))

(perc.se <- (ub-forecast$pred)/1.96/forecast$pred)

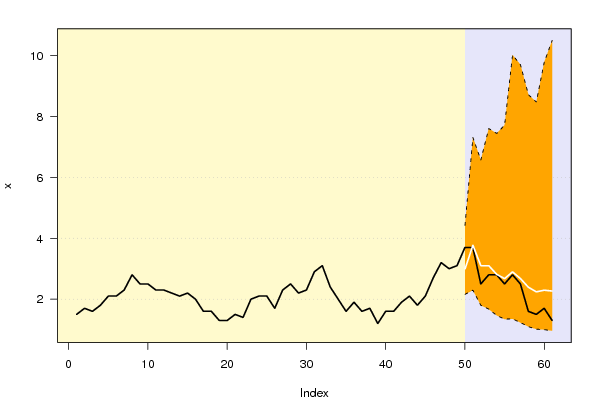

bitmap(file='test1.png')

opar <- par(mar=c(4,4,2,2),las=1)

ylim <- c( min(x[first:nx],lb), max(x[first:nx],ub))

plot(x,ylim=ylim,type='n',xlim=c(first,lx))

usr <- par('usr')

rect(usr[1],usr[3],nx+1,usr[4],border=NA,col='lemonchiffon')

rect(nx1,usr[3],usr[2],usr[4],border=NA,col='lavender')

abline(h= (-3:3)*2 , col ='gray', lty =3)

polygon( c(nx1:lx,lx:nx1), c(lb,rev(ub)), col = 'orange', lty=2,border=NA)

lines(nx1:lx, lb , lty=2)

lines(nx1:lx, ub , lty=2)

lines(x, lwd=2)

lines(nx1:lx, forecast$pred , lwd=2 , col ='white')

box()

par(opar)

dev.off()

prob.dec <- array(NA, dim=fx)

prob.sdec <- array(NA, dim=fx)

prob.ldec <- array(NA, dim=fx)

prob.pval <- array(NA, dim=fx)

perf.pe <- array(0, dim=fx)

perf.mape <- array(0, dim=fx)

perf.mape1 <- array(0, dim=fx)

perf.se <- array(0, dim=fx)

perf.mse <- array(0, dim=fx)

perf.mse1 <- array(0, dim=fx)

perf.rmse <- array(0, dim=fx)

for (i in 1:fx) {

locSD <- (ub[i] - forecast$pred[i]) / 1.96

perf.pe[i] = (x[nx+i] - forecast$pred[i]) / forecast$pred[i]

perf.se[i] = (x[nx+i] - forecast$pred[i])^2

prob.dec[i] = pnorm((x[nx+i-1] - forecast$pred[i]) / locSD)

prob.sdec[i] = pnorm((x[nx+i-par5] - forecast$pred[i]) / locSD)

prob.ldec[i] = pnorm((x[nx] - forecast$pred[i]) / locSD)

prob.pval[i] = pnorm(abs(x[nx+i] - forecast$pred[i]) / locSD)

}

perf.mape[1] = abs(perf.pe[1])

perf.mse[1] = abs(perf.se[1])

for (i in 2:fx) {

perf.mape[i] = perf.mape[i-1] + abs(perf.pe[i])

perf.mape1[i] = perf.mape[i] / i

perf.mse[i] = perf.mse[i-1] + perf.se[i]

perf.mse1[i] = perf.mse[i] / i

}

perf.rmse = sqrt(perf.mse1)

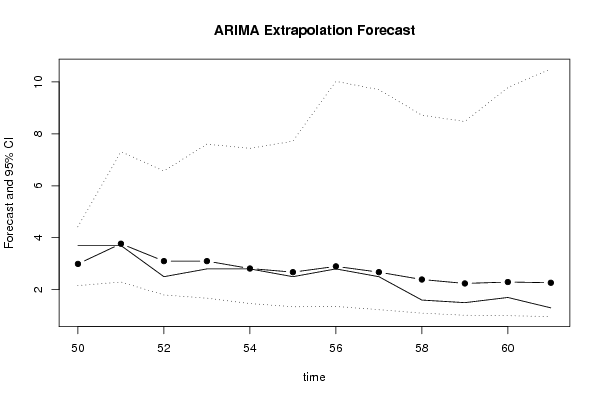

bitmap(file='test2.png')

plot(forecast$pred, pch=19, type='b',main='ARIMA Extrapolation Forecast', ylab='Forecast and 95% CI', xlab='time',ylim=c(min(lb),max(ub)))

dum <- forecast$pred

dum[1:par1] <- x[(nx+1):lx]

lines(dum, lty=1)

lines(ub,lty=3)

lines(lb,lty=3)

dev.off()

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Univariate ARIMA Extrapolation Forecast',9,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'time',1,header=TRUE)

a<-table.element(a,'Y[t]',1,header=TRUE)

a<-table.element(a,'F[t]',1,header=TRUE)

a<-table.element(a,'95% LB',1,header=TRUE)

a<-table.element(a,'95% UB',1,header=TRUE)

a<-table.element(a,'p-value

(H0: Y[t] = F[t])',1,header=TRUE)

a<-table.element(a,'P(F[t]>Y[t-1])',1,header=TRUE)

a<-table.element(a,'P(F[t]>Y[t-s])',1,header=TRUE)

mylab <- paste('P(F[t]>Y[',nx,sep='')

mylab <- paste(mylab,'])',sep='')

a<-table.element(a,mylab,1,header=TRUE)

a<-table.row.end(a)

for (i in (nx-par5):nx) {

a<-table.row.start(a)

a<-table.element(a,i,header=TRUE)

a<-table.element(a,x[i])

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.element(a,'-')

a<-table.row.end(a)

}

for (i in 1:fx) {

a<-table.row.start(a)

a<-table.element(a,nx+i,header=TRUE)

a<-table.element(a,round(x[nx+i],4))

a<-table.element(a,round(forecast$pred[i],4))

a<-table.element(a,round(lb[i],4))

a<-table.element(a,round(ub[i],4))

a<-table.element(a,round((1-prob.pval[i]),4))

a<-table.element(a,round((1-prob.dec[i]),4))

a<-table.element(a,round((1-prob.sdec[i]),4))

a<-table.element(a,round((1-prob.ldec[i]),4))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Univariate ARIMA Extrapolation Forecast Performance',7,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'time',1,header=TRUE)

a<-table.element(a,'% S.E.',1,header=TRUE)

a<-table.element(a,'PE',1,header=TRUE)

a<-table.element(a,'MAPE',1,header=TRUE)

a<-table.element(a,'Sq.E',1,header=TRUE)

a<-table.element(a,'MSE',1,header=TRUE)

a<-table.element(a,'RMSE',1,header=TRUE)

a<-table.row.end(a)

for (i in 1:fx) {

a<-table.row.start(a)

a<-table.element(a,nx+i,header=TRUE)

a<-table.element(a,round(perc.se[i],4))

a<-table.element(a,round(perf.pe[i],4))

a<-table.element(a,round(perf.mape1[i],4))

a<-table.element(a,round(perf.se[i],4))

a<-table.element(a,round(perf.mse1[i],4))

a<-table.element(a,round(perf.rmse[i],4))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable1.tab')

|